Traceloans.com appears to be a finance content site, not a clearly identified direct lender. Use it for research, then verify any lender, rates, fees, and licensing before sharing personal information.

That distinction matters. The homepage is built around articles and category pages, not around a visible loan application flow or rate-comparison engine. Recent posts focus on debt validation, loan forbearance, and other educational topics, and the visible categories include Debt Management, Personal & Consumer Loans, and Unsecured Personal Loans.

What Traceloans.com actually is

Based on the live site, Traceloans.com looks more like a publishing platform that explains borrowing topics than a lender making direct credit offers. The branding line on the homepage is “Demystifying Loans for Every Milestone,” and the content mix is editorial. That makes the site useful for orientation, but it should not be mistaken for a binding loan offer.

This is where weaker review pages miss the mark. They ask whether the site is “legit” without first classifying the business model. If a site is primarily informational, the right review standard is accuracy, transparency, and whether it points users toward regulated providers.

How the site presents itself right now

The homepage highlights fresh March 2026 content, including articles on old collection accounts and forbearance. That signals an active editorial site, not a dead placeholder. It also shows a topical focus on consumer debt and borrowing decisions.

What I do not see on the search-visible homepage is also important. There is no obvious evidence in the parsed homepage of direct lender disclosures, a lender license number, or a front-and-center application funnel. That does not prove the site is unsafe. It does mean users should verify the site’s role before treating it like a lender.

Is Traceloans.com legit?

Legit and safe are not the same question. A site can be legitimate as a publisher and still be the wrong place to submit sensitive data if it does not clearly explain who is collecting it, why it is needed, and what happens next.

A practical standard is simple. If a site discusses loans, it should make the commercial relationship clear. If it refers users elsewhere, that should be disclosed. If it touches mortgage products, users should be able to verify the company or professional through NMLS Consumer Access, which the CFPB identifies as a free tool for checking whether a person or company is permitted to make or broker mortgage loans.

What smart users should verify before trusting any loan site

The APR matters more than the headline interest rate because APR captures interest plus certain fees. The CFPB states that APR is one of the most important measures of borrowing cost, and it is the number serious shoppers should compare first.

You should also check whether fees are disclosed before moving forward. The CFPB says borrowers should review origination charges and other loan costs, not just the advertised rate. That applies whether you found the offer through Traceloans.com or anywhere else.

Then verify the firm’s licensing and identity. For mortgage products, the CFPB points consumers to NMLS Consumer Access. For suspicious outreach, the FTC warns that scammers often use unexpected messages, false preapproval claims, and requests for personal or bank information to push fast decisions.

Quick comparison: content site vs direct lender

| Checkpoint | Traceloans.com appears to be | What a direct lender should show |

|---|---|---|

| Core function | Educational loan content | Loan products and application path |

| Homepage focus | Articles and categories | Rates, terms, eligibility, disclosures |

| Trust review | Accuracy and transparency | Licensing, fees, underwriting |

| User action | Research and verify | Compare, prequalify, apply carefully |

This is the real user journey. Use Traceloans.com to learn the language of borrowing, but make your decision only after you verify the actual lender’s APR, fees, terms, and regulatory status.

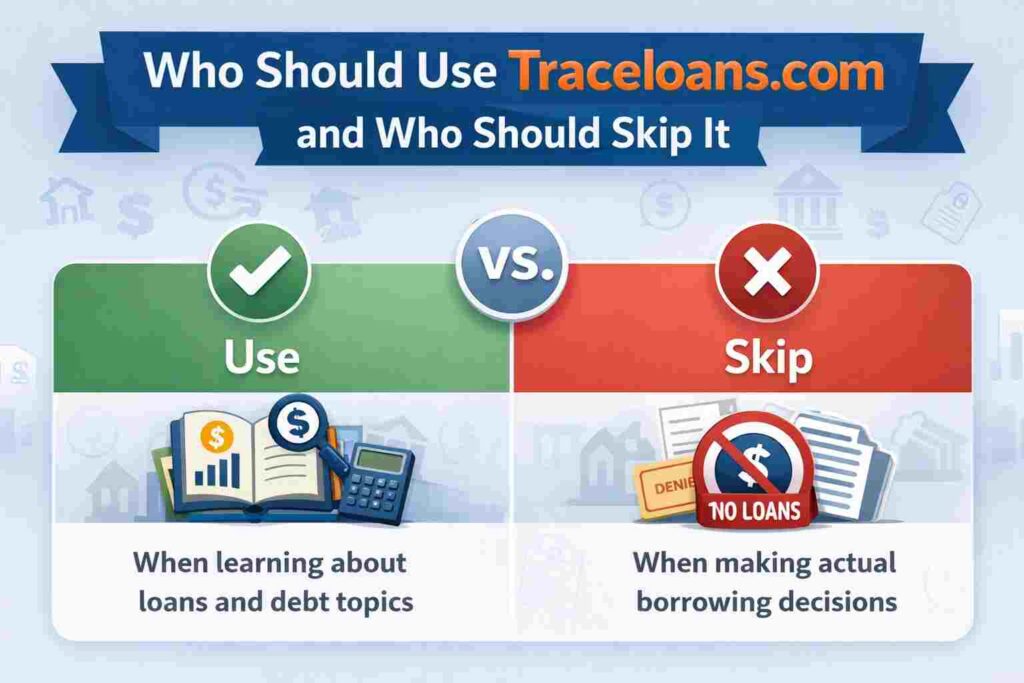

Who should use Traceloans.com and who should skip it

Use the site if you need a starting point on debt management, personal loans, or loan basics. The current content shows active publishing, and some topics reflect real borrower concerns.

Skip it as your final decision point. If you are about to submit an application, compare offers through regulated lenders or marketplaces that clearly disclose fees, terms, and licensing. Education is useful. Verification is mandatory.

Bottom line

Traceloans.com is best treated as a research resource, not as a lender you should trust by default. Read the guides, then confirm every loan detail with the actual provider. That one step protects your credit, your data, and your leverage.

FAQs

Is Traceloans.com a direct lender?

The live site looks primarily editorial. I would not assume it is a direct lender unless the company clearly states that role and provides the required disclosures.

Is Traceloans.com safe to use?

It may be safe to read, but do not share sensitive information until you know who is collecting it, how it is used, and whether the provider is properly licensed.

What should I compare before applying?

Compare APR, total fees, repayment term, monthly payment, and whether the lender is licensed for the product and state involved.

How can I verify a mortgage company?

Use NMLS Consumer Access. The CFPB recommends it as a free way to check whether a company or professional is permitted to make or broker mortgage loans.